How much can your business borrow?

By

Aurora Capital

April 7, 2026

.svg)

.svg)

If you’re looking for a loan to help fund and grow your business, it’s important to understand how much money you could potentially borrow.

Like personal finance, your business’s credit history and financial performance will determine what you can borrow.

However, by understanding your business’s borrowing capacity and what lenders base their lending decisions on, you can get a good idea of what you could access.

What factors determine how much your business can borrow?

Six main factors are considered by lenders when determining how much they could lend you.

Revenue and profit

The first thing lenders will look at when determining how much you can borrow for your business is your revenue.

Most lending companies offer a set percentage of your annual turnover or, for young businesses, a multiplication of your monthly revenue. For example:

- 40% of your annual turnover - so. If your turnover is £500,000, you could borrow up to £200,000

- 1.5x your monthly revenue - so, if your revenue is £40,000, you could borrow up to £60,000

Lenders will also want to check that your turnover has grown or been steady over the last six months. This will give them confidence that your business is stable.

Some lenders stipulate that your business must not be in financial difficulty before they will lend to you, but others aren’t quite so strict. However, the more profitable your business is, the better your chance of getting approved for a loan and the more you can borrow.

If your business is struggling, you could still get the loan you need if you can show that it will be used as a catalyst for growth.

Current debts and commitments

Lenders will look at any existing debts your business has to help them determine whether you can afford the loan you’re applying for.

They look at outstanding loans, regular expenses, and fixed overhead costs to gauge your ability to take on new debt without overextending your finances. Key factors that lenders consider include:

- Debt-to-income ratio (DTI): This compares your total monthly debt payments to your monthly revenue. A lower ratio indicates a healthier financial position, making it easier to secure larger loans.

- Existing loan repayments: If your business is already repaying multiple loans, lenders may limit the amount they offer to prevent excessive debt burdens.

- Operational expenses: High fixed costs (such as rent, salaries, and utilities) reduce the disposable income available to service new loans, potentially lowering borrowing capacity.

- Cash flow: Lenders assess whether your revenue consistently covers existing expenses and potential new repayments. Businesses with fluctuating income may face stricter borrowing limits.

To improve your borrowing capacity, aim to maintain a manageable level of debt to ensure you have enough free cash flow to support additional financing.

Collateral

Collateral, like property, vehicles, stock, or equipment, can help boost the amount you can borrow.

Certain types of loans, like secured business loans, require collateral to secure the loan against. Secured loans typically allow you to borrow more because the risk to the lender is reduced. If you default on the loan, they can use the collateral to recoup the outstanding balance so they won’t be out of pocket.

On the other hand, unsecured business loans don’t require collateral, but the risk to the lender is increased. Therefore, the amount you can borrow is less.

The amount you can borrow will be partly determined by the value of your assets. The higher the value of the assets you have, the more lenders can recover if you default on payments, and therefore, the more they’re willing to let you borrow for your business.

Personal guarantee

Personal guarantees are often required when a lender has no property or assets to secure the loan against.

A personal guarantee is an agreement in which a business owner or director personally accepts liability for repaying the loan if the business is unable to do so.

A strong personal guarantee can increase the amount your business can borrow and improve your chances of getting a loan. Factors that influence the strength of a personal guarantee include:

- Your personal credit score

- Personal assets, e.g., the value of any property you own

- Existing personal debt

Being a homeowner is considered an important factor when providing a personal guarantee, and it greatly impacts what you can borrow.

Credit score

Your business credit score can play a crucial role in determining how much you can borrow. A strong score indicates to lenders that your business is financially stable and manages credit reliably.

Therefore, the better your credit score, the more you can borrow and the better your chances of getting approved. However, not every business has a good credit score, especially newer businesses.

Credit scores take time to build up and can generally be improved by taking out credit and showing that you can pay it off. This is why a low credit score won’t necessarily stop your business from getting credit, but it may mean you can’t borrow as much as you need.

Down payment

Making a down payment can significantly improve your borrowing power and loan terms when securing finance for equipment, machinery, or other business assets.

While some lenders offer 100% financing, contributing an upfront payment demonstrates financial commitment and reduces risk for the lender. This can result in lower interest rates, higher borrowing limits, and more flexible repayment options, especially when applying for asset finance.

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

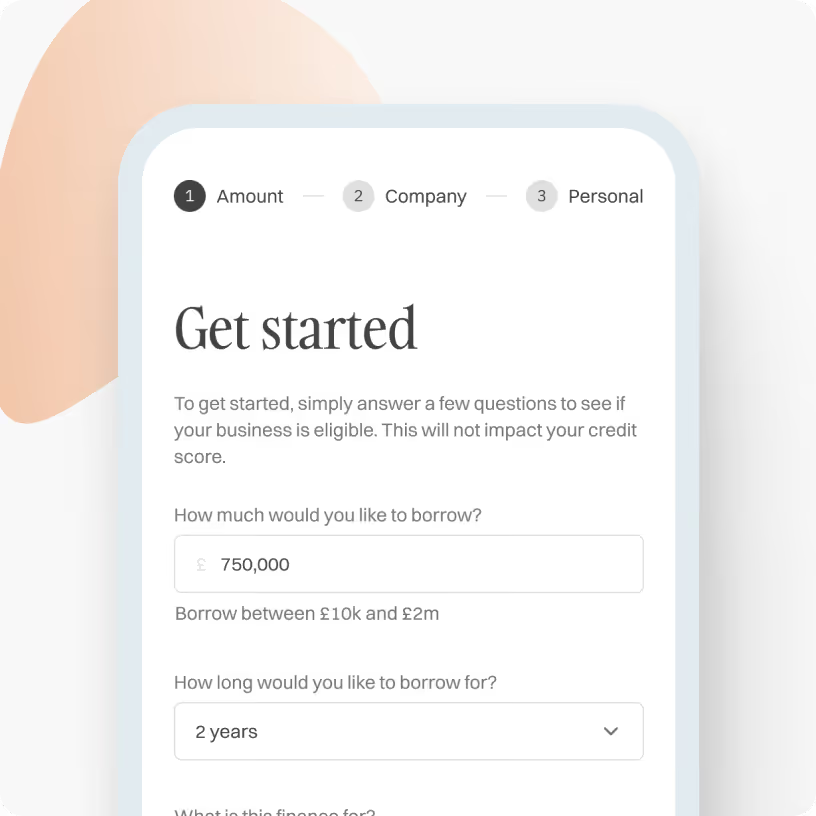

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Frequently asked questions

How to maximise your borrowing potential

Making sure your business can borrow as much as possible needs careful financial management and a strategic approach to your application.

By strengthening your credit profile and demonstrating financial stability, you can improve your chances of borrowing more.

Build a strong credit profile

Lenders assess your business credit score to determine risk. To improve your creditworthiness:

- Pay all invoices, loan repayments, and supplier accounts on time

- Reduce outstanding debts and avoid maxing out credit limits

- Monitor your business credit report and correct any inaccuracies

A strong credit profile can help you access higher loan amounts and potentially more competitive interest rates.

Demonstrate financial stability

Consistent revenue and profit growth show lenders that your business can manage repayments. To strengthen your financial position:

- Maintain stable cash flow and avoid large fluctuations in income

- Keep overheads manageable and demonstrate efficient cost control

- Prepare up-to-date financial statements, including profit and loss reports and balance sheets

Lenders look favourably on businesses with strong financial track records and predictable income streams.

Explore how we helped a website design company secure £30,000 in working capital to support growth in this case study.

Borrowing limits of different loan types

Asset finance

Asset finance allows businesses to purchase or lease equipment, spreading costs over time. Asset finance doesn’t tend to have a specific limit because of the fluctuation in the price of goods, but you could potentially borrow:

- Up to 100% of asset value, depending on depreciation

- Loan amounts typically range from £1,000 to £1 million.

When financing assets, several options include going directly through the manufacturer or through a private lender.

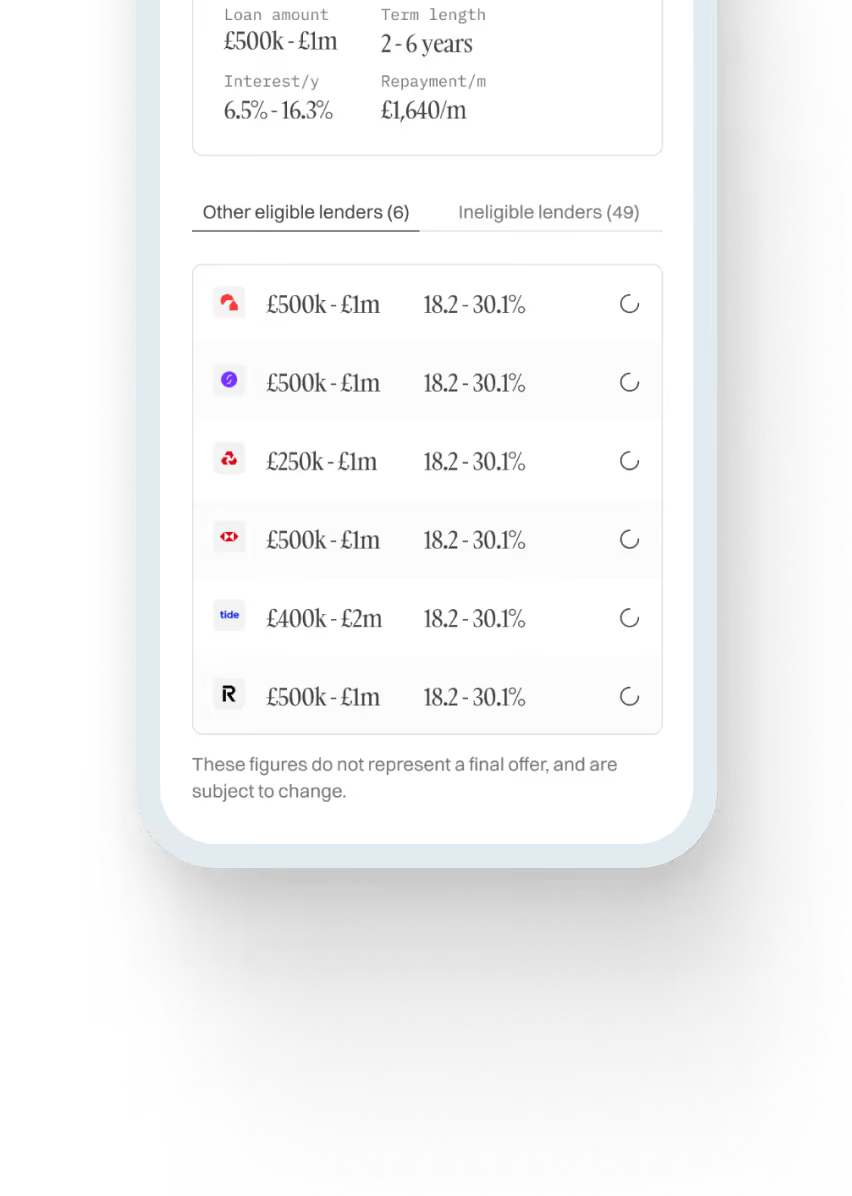

Unsecured business loans

There are over 50 lenders that offer unsecured business loans, and each lender has a slightly different way of calculating how much you can borrow. However, there are three main approaches:

- Turnover: Some lenders will offer up to 40% of your annual turnover in your last filed accounts.

- Monthly revenue: Other lenders will look to lend up to 1.5x your average monthly turnover in the last 6 months.

- EBITDA: Some lenders may offer loans of up to three times your EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortisation).

The maximum you can borrow with an unsecured business loan is usually capped at £500,000, regardless of your business’s financial performance.

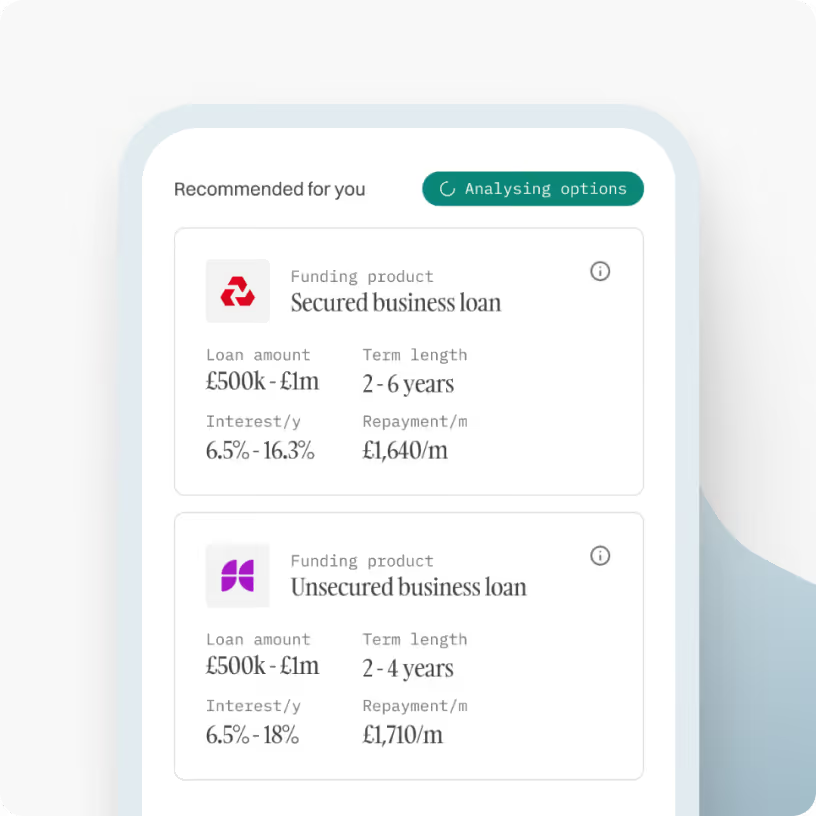

Secured business loans

Secured business loans are based on the available equity in your property or properties you are willing to use as collateral. Typically, borrowing limits for secured loans are:

- Up to 75% LTV (loan-to-value) of the asset used as security

- Loan amounts range from £25,000 to £2 million

For example, if you have a property worth £500k and a mortgage of £200k, the maximum you can borrow would be £175k. This is calculated by calculating 75% of the property value and then subtracting the existing mortgage.

Merchant cash advance

A merchant cash advance (MCA) provides funding based on future credit and debit card sales. You repay the loan through a percentage of your daily transactions, making it a flexible option for those with fluctuating incomes.

Here’s what you could potentially borrow using an MCA:

- Up to 150% of your average monthly card sales

- Loans available typically range from £5,000 to £500,000

For example, if you have been trading for 10 years and your card sales are £50,000 per month, you could potentially borrow up to 150% of this, £75,000.

However, if you have only been trading for 12 – 24 months, you are more likely to be offered something closer to 100% of your monthly card sales.

Understanding your business's borrowing capacity

It’s important to understand your business’s borrowing capacity. Borrowing capacity isn’t just about how much money your company could get from lenders but also about how much you should be borrowing.

For example, you may be able to borrow up to £200,000, but you might work out that you can only afford £130,000 based on the cost of your monthly payments. This prevents you from taking out more money than you can reasonably pay back and afford without affecting your cash flow even further.

Some lenders might agree to let you borrow up to 40% of your annual turnover, but that doesn’t mean you should decide to borrow that much. Borrowing capacity is all about borrowing sustainable and viable amounts of money you can pay back, not just in the short term but in the long term.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)