Our LendTech platform lets you:

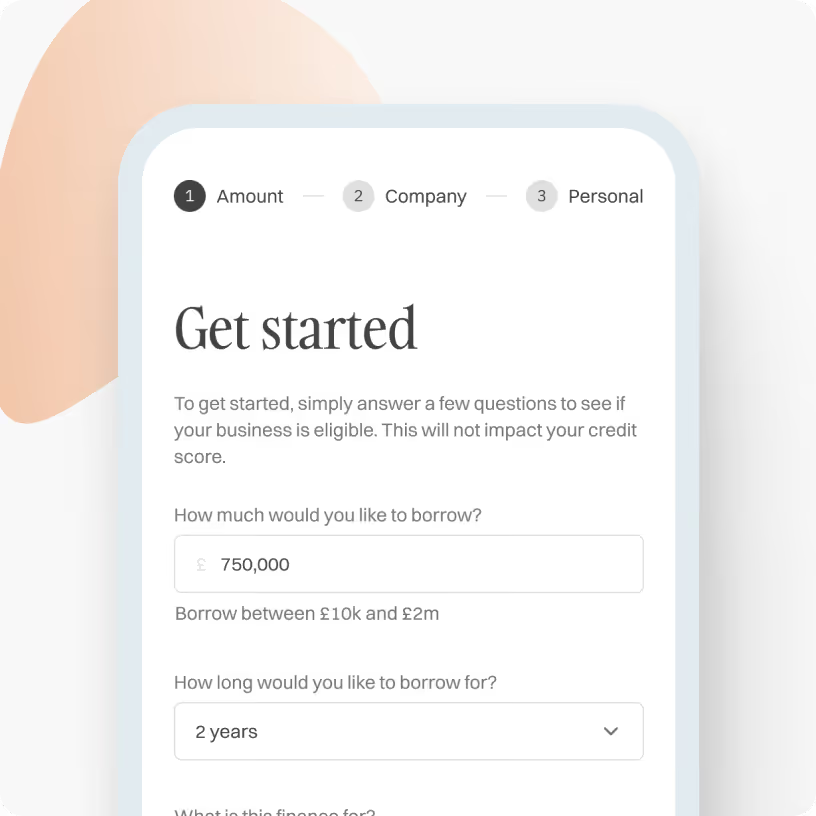

Check eligibility in 30 seconds

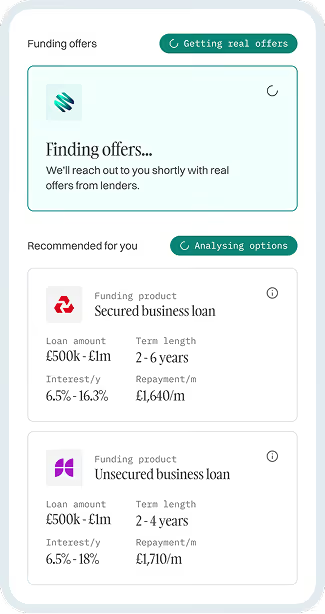

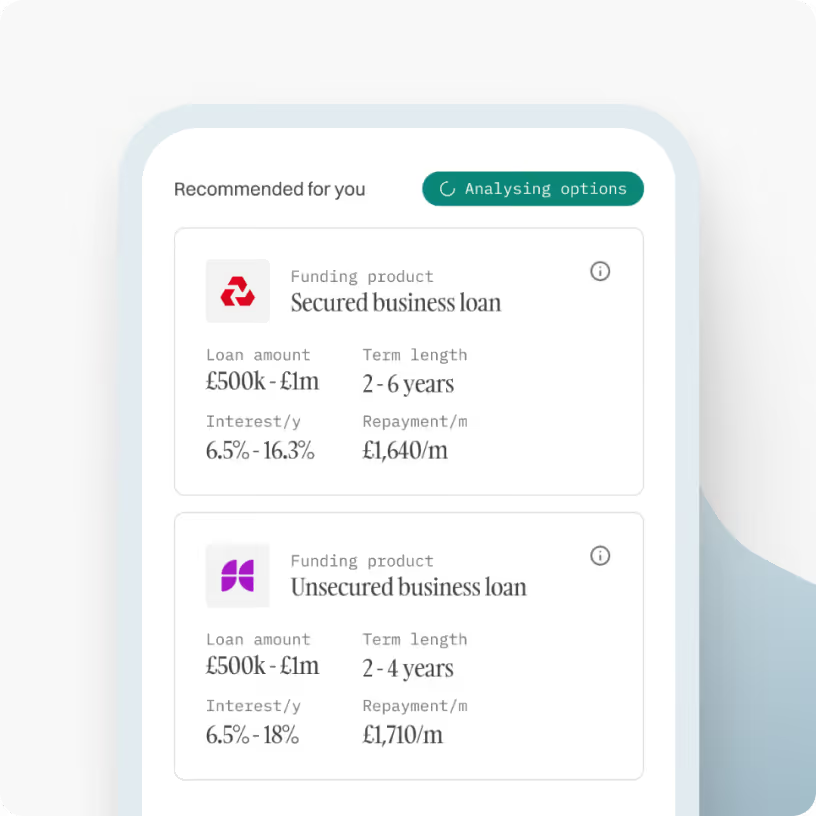

Match with 50+ lenders

Get indicative offers in 5 mins

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

What is an unsecured business loan?

Unsecured business loans allow your business to borrow without using any tangible assets as security. This means that the loan will not be directly linked to any business or personal assets if you default on your loan.

They are usually a much quicker and easier option than a secured loan because the lender doesn’t need to evaluate and value any potential security assets.

However, because they can be riskier for lenders, they can be slightly more expensive, and the maximum loan is capped at £500k. However, unsecured business loans are more suited to the SME market where businesses are looking to borrow between £10k and £500k.

.svg)

Key features

- Suitability: Ideal for businesses looking for short to medium-term financing without using an asset as collateral.

- Purpose: They can be used for most business purposes, including stock purchases, boosting cash flow, growth or refinancing debt.

- Amount: Unsecured loans typically range from £10k to £500k. How much you can borrow can be based on a percentage of your turnover or a multiple of profit.

- Term: Loan terms available between 1 month and 6 years.

- Cost: Interest rates vary depending on the lender, but rates start from 8.9%.

How do unsecured business loans work?

An unsecured business loan provides your business with a one-off lump sum that you repay via fixed monthly payments. You'll pay back the loan over a set time period, usually between 1 and 6 years, and pay interest on what you've borrowed.

You can use an unsecured business loan for almost any reason, as long as it's a legitimate business expense. Common uses of an unsecured business loan include:

- Cash flow

- Stock purchase

- Business growth

- Refurbishment

- Settling bills

- Refinancing debts

Unsecured loans can be slightly more expensive than secured loans because they are seen as a higher risk. There is no tangible security for the lender, although a personal guarantee may be required, to fall back on if you're unable to repay the loan, so they tend to charge a higher interest rate and offer lower loan amounts.

Is your business eligible for an unsecured business loan?

When you apply for a loan, the lender will assess your business to determine whether or not you qualify. They need to be confident that you can afford to repay what you borrow, so they check things like:

- Your borrowing history

- Your business credit report

- Your current debts

- Your revenue

This will give them a clearer picture of how reliable your business is and how well you've managed credit in the past. They will also have general eligibility criteria, typically including:

- You're over 18 years old

- The business has been trading for at least three months and has a turnover of more than £8k per month

- The business is trading and registered in the UK

- Your business has a UK business bank account

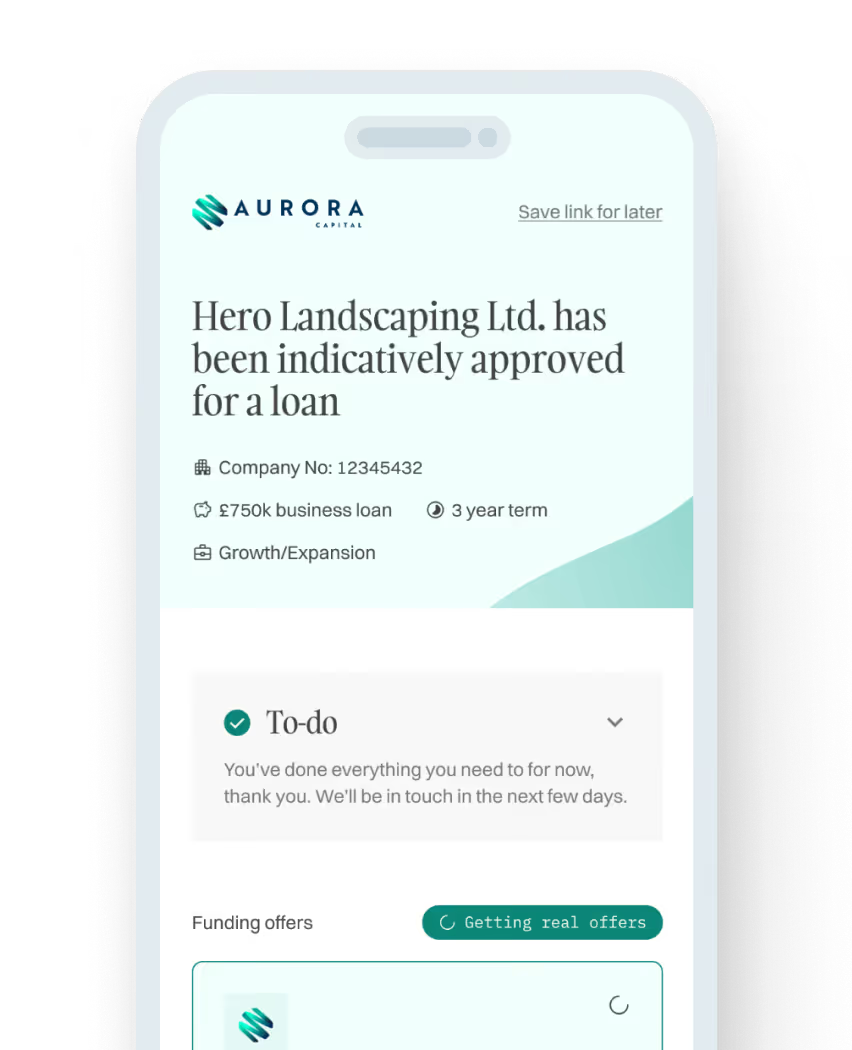

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

.svg)

Frequently asked questions

Pros and cons of unsecured business loans

Unsecured business loans are a common way to raise funding, but they might not be suitable for your company. Weigh up the pros and cons to help you determine if they could be the best option.

Pros of unsecured business loans

- No security needed: Your business doesn’t need to have any high-value assets like property, land, or equipment to use as collateral, making it an attractive option for new or small businesses. However, a personal guarantee may be required.

- No risk to assets: As you don’t put any tangible assets down as security, there is no risk you’ll lose them if you’re unable to keep up with your loan repayments.

- Quicker and easier: The application process can be more straightforward because the lender won’t need to value and evaluate your assets.

- No early repayment costs: There are usually no early settlement penalties for unsecured loans.

- Easy budgeting: Paying a fixed monthly repayment for a set term makes it easier for your business to manage and budget the cost.

Cons of unsecured business loans

- Higher interest rates: Unsecured loans usually have slightly higher interest rates to offset the lender's increased risk because they have no assets to repossess if you can’t repay the loan.

- Small loan amounts: Due to the increased level of risk, lenders tend to offer lower loan amounts compared to secured business loans. However, most of our lenders can still lend up to £500k.

- Stricter eligibility: Lenders set tougher eligibility requirements because they need to be confident that your business can make the repayments, as having no security increases the risk.

- Personal guarantee: Some lenders may ask for a personal guarantee in place of the security of an asset. This means you will be personally responsible for the debt if your business fails.

Alternatives to unsecured business loans

If you’re unsure whether an unsecured loan is the right funding option for your business, there are several alternatives you could consider.

- Secured business loans: This type of loan allows you to borrow more over a longer period and at a lower interest rate. You need to provide a valuable asset as security.

- Bridging loans: A business bridging loan is designed to bridge a gap between a big purchase and an influx of money. It’s a secured loan designed to be taken out for a short period.

- Asset finance: This type of business finance allows you to purchase a new asset and spread the cost over time.

- Revolving credit line: This works in a similar way to an overdraft or credit card and gives you instant access to credit as and when your business needs it.

- Invoice finance: This allows you to access money tied up in your unpaid invoices, allowing you to operate while you wait for payment.

- Merchant cash advance: This allows you to borrow against future card transactions. You repay a fixed percentage of your card sales until the loan is repaid.

- Peer-to-peer lending: Peer-to-peer lending works by connecting investors with businesses directly via an online platform.

Unsecured vs secured business loans

The main difference between secured and unsecured business loans is that secured loans use your assets as security, and unsecured loans do not.

Which option is right depends on how much you need to borrow and what assets your business owns. A secured loan could be the best option if you own valuable assets, like property, and need to borrow a large sum. Here’s an overview of how the two types of loans compare:

Unsecured loanSecured loanSecurity requiredNoYesCredit historyGood score requiredLow score consideredInterest rateFrom 8.9% Lower rates availablePersonal guaranteeMay be requiredMay be requiredTime to acquireWithin 48 hoursIt can take up to 6 weeks

See how we helped a security company secure a £23,000 unsecured loan in this case study.

How much can I borrow on an unsecured loan?

All lenders work slightly differently from each other, but most will either lend on a percentage of your turnover or a multiple of profit. Usually, they will only lend a maximum of 40% of annual turnover. So, if your annual revenue is £500,000, you will be able to borrow up to £200,000.

Lenders will look into your historical financial data and your credit profile to assess your affordability. Loans typically range from £1k – £500k.

Are small business loans secured or unsecured?

Small business loans can be secured or unsecured. However, small businesses are more likely to qualify for an unsecured loan as they might not have the necessary assets to use as collateral for a secured loan.

Can a start-up business get an unsecured loan?

It is not possible for a start-up business to get an unsecured loan. Unsecured lenders like to see businesses trading for longer than four months before they assess a proposal.

If the business hasn’t started trading yet or requires a larger investment, a secured business loan may be better suited for you.

How much does an unsecured business loan cost?

This will vary from lender to lender, but you can expect interest rates to start from 8.9% annually. What interest rate you get can also depend on your business’s credit rating and affordability checks.

Some lenders may also charge an admin fee – this will be a percentage of the loan amount and will likely be deducted from the loan, so there is no need for any upfront fees to be paid.

What can an unsecured business loan be used for?

An unsecured business loan can be used for almost any purpose, provided it is for legitimate business purposes. Common reasons businesses get unsecured loans include buying stock, refurbishing, cash flow, settling bills, and refinancing debts.

Can I get an unsecured business loan with bad credit?

Getting an unsecured loan is possible if your business has a poor credit rating, but it will be much more difficult. Unsecured loans are considered more risky for lenders, so they will need to be confident your business can afford the loan.

They can determine this by checking your credit score to see how you’ve managed credit in the past. If you have a low credit score, they may consider your application if you also provide a personal guarantee.

Does an unsecured business loan need a personal guarantee?

Most unsecured loans require a personal guarantee to secure the facility, however, the lender will always try to work with you before enforcing this.

What happens if you default on an unsecured business loan?

If you’re unable to meet your loan repayments, your business may face a number of consequences. You may incur late or missed payment fees, your credit score will be damaged, and the lender may need to take legal action to recover the debt.

If you agree to a personal guarantee as part of your application, you will be liable for the debt. That means you may have to cover the losses personally, and your assets may be at risk.

How quickly can I get an unsecured business loan?

When you apply with Aurora Capital, we can give you a decision in as little as 24 hours, and you could even be in receipt of the funds within 48 hours.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

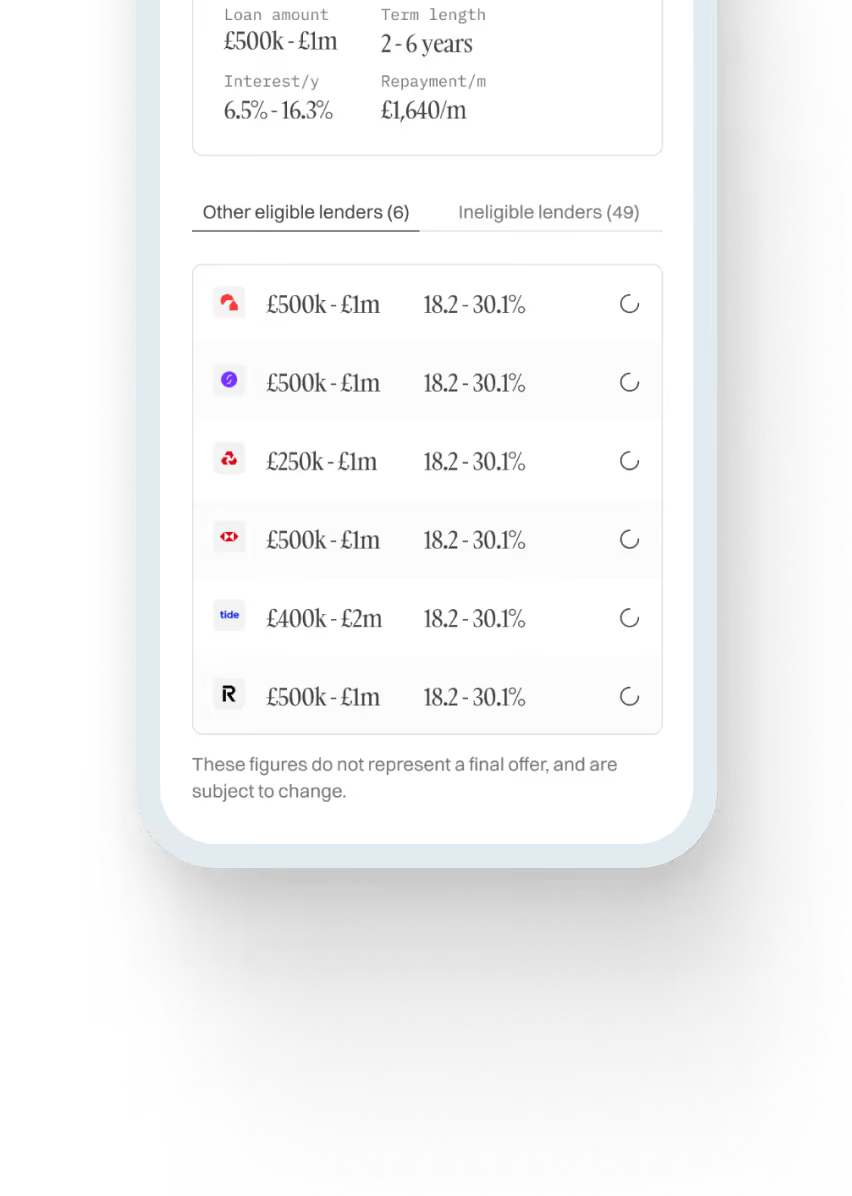

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Get a quote, fast

Lending period

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

Guides to help you make the best financial decisions

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)