Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

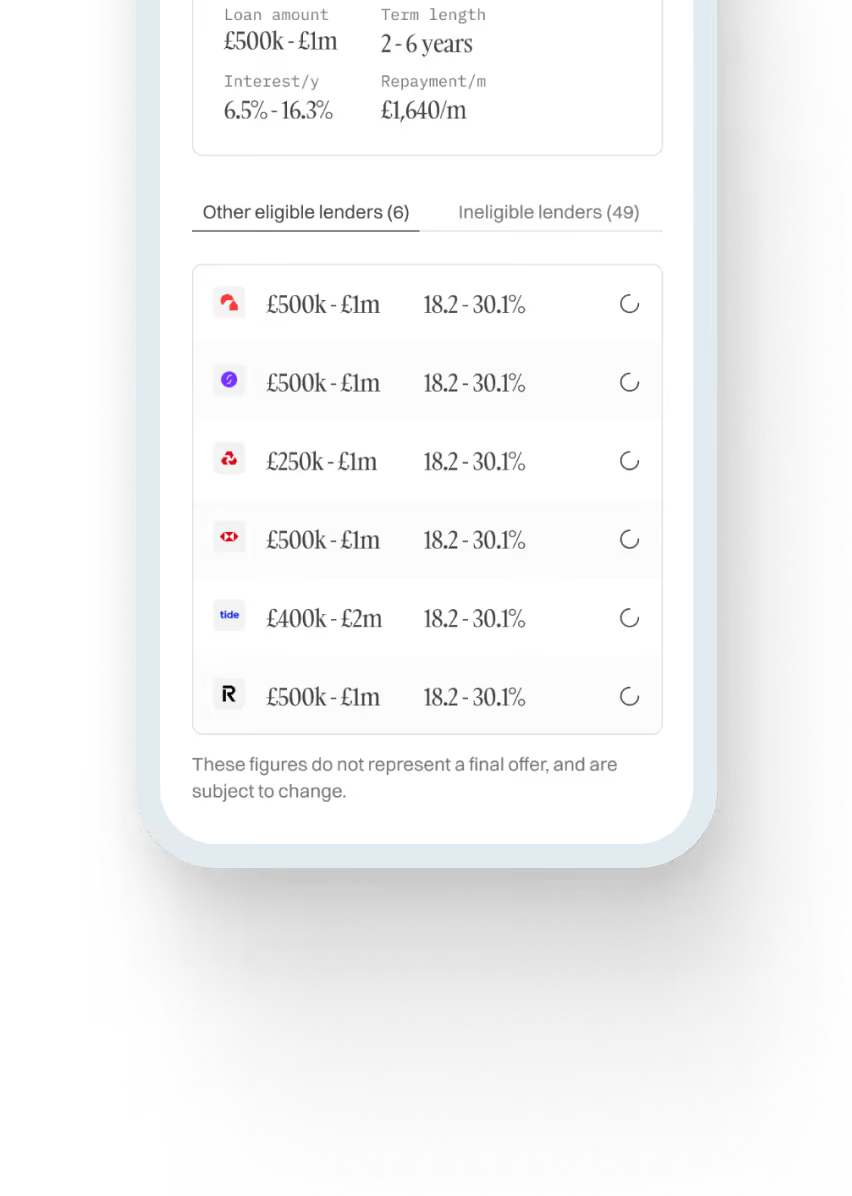

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

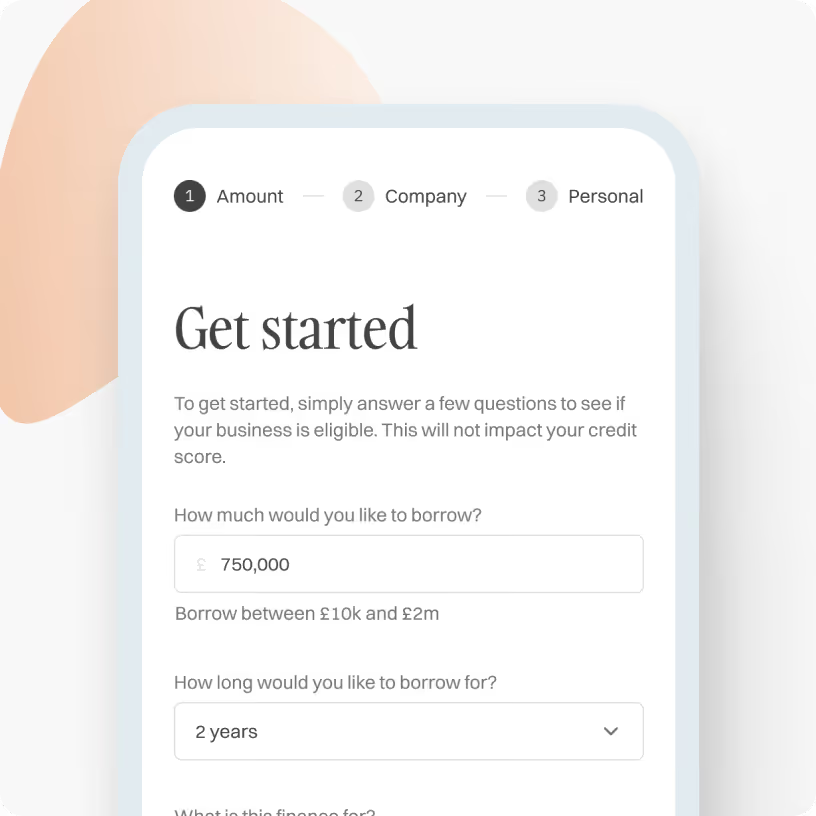

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

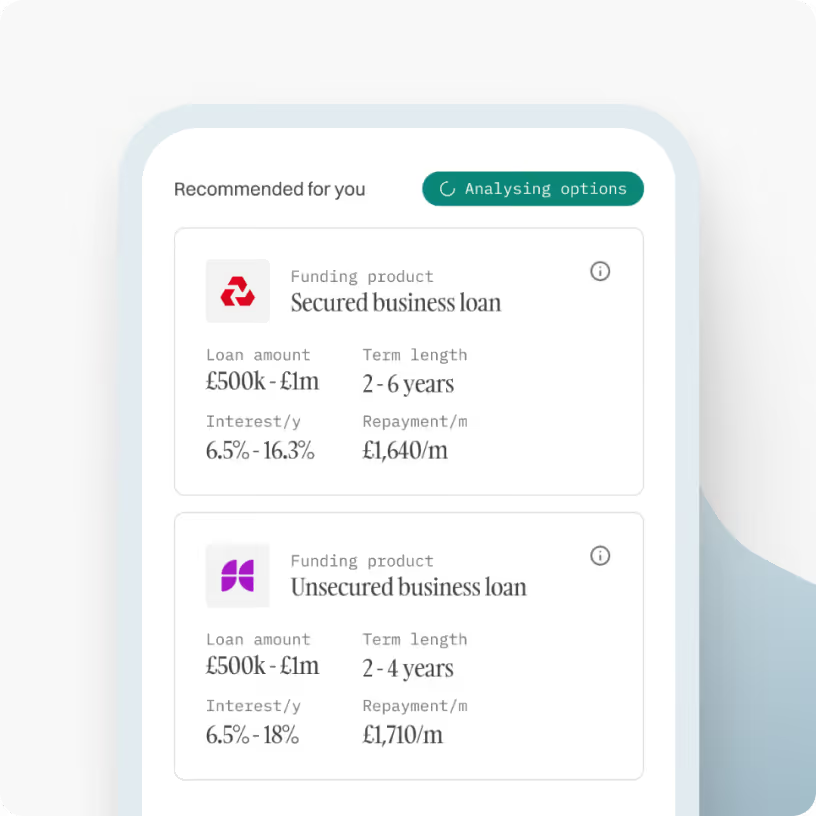

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

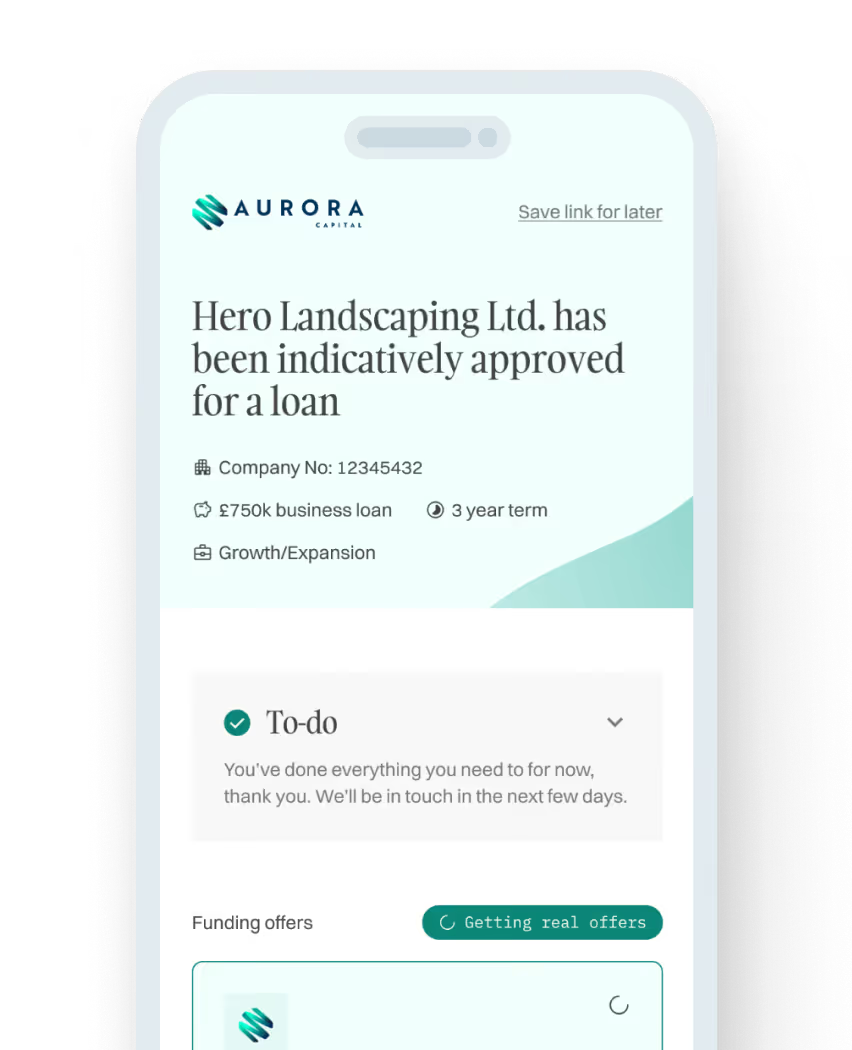

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Guides to help support all sorts of UK businesses

Business Loans

Cashflow Loans

Asset Finance

Frequently asked questions

What is a business loan?

Business loans are a way of borrowing money to support or grow your business. They are specifically designed to meet the financial needs of businesses, from startups to established companies.

You can get a business loan from high-street banks, online lenders and other financial institutions. Which is right for you will depend on your business’s needs – when you apply with Aurora Capital, you can compare funding options to find the right loan for you

How does a business loan work?

They work in a similar way to personal loans. You apply to borrow money from a lender, which you agree to repay over time with interest or a fixed fee.

The funds must be used for business purposes, and you will need to provide information about your company as part of the application process.

Whether or not your application will be successful will depend on factors such as your business credit score, annual revenue, annual profit, the value of any assets you have, bank account conduct and the length of time your company has been trading.

As with any loan, you must keep up with your monthly repayments. Failure to do so could damage your business credit score and result in assets being repossessed or court action, depending on the type of loan you choose.

Types of business loans

There is a range of different business loan types you can choose from. Which option is right for your business will depend on what you need the funds for, the type of company you run and the size of the business.

Here are some of the business funding options you can choose from:

- Unsecured business loans: This is a loan that does not need to be secured against a business asset, which reduces the risk, but they are usually more expensive than other options.

- Secured business loans: A secured business loan requires you to use something like property or equipment as collateral. This means an asset is at risk if you don’t keep up with your repayments.

- Asset finance: This type of borrowing is designed to help a business buy new or used assets like equipment, vehicles, or machinery and spread the cost over time. This can be done through leasing or hire purchase agreements.

- Merchant cash advance: A merchant cash advance is a way of accessing finance in exchange for an agreed percentage of your future sales through credit or debit card transactions.

- Revolving credit line: This is a line of credit that allows your business to access funds up to a set limit as and when you need them.

- Invoice finance: This is a way for businesses to borrow against unpaid invoices and immediately access up to 90% of the invoice's value.

- Growth guarantee scheme (formerly the Recovery Loan Scheme): This government-backed scheme is designed to help small UK companies access the finance they need through an unsecured business loan.

- Bridging loans: A business bridging loan is a way of accessing short-term finance to cover a gap between current debt and incoming cash flow, by securing on a UK residential or commercial property.

- Peer-to-peer lending: A peer-to-peer business loan connects a business with individual investors willing to lend to them. Businesses and investors are connected through dedicated online platforms.

How can I use a business loan?

You can use a business loan for anything your company needs in order to operate or expand. Common uses for business finance include:

- Purchasing new equipment like tools or machinery

- Moving to bigger premises

- Employing more staff

- Buying more stock

- Increasing your marketing

- Consolidating your existing debts

- Covering running costs

- Improving short-term cash flow

It’s important to remember that a business loan can only be used for the benefit of your company. Some lenders will ask you what the funds are for as part of your application.

How to get a business loan

Here are the steps you need to follow to apply for a UK business loan:

- Work out how much you need to borrow and what repayments you can afford.

- Consider which type of loan is right for your needs.

- Check your business credit score and take steps to improve it if necessary.

- Get together all the documents you need to provide as part of the application.

- Find and compare funding options with Aurora Capital today.

Use our business loan calculator below to help you understand how much a loan could cost your business and how much you can afford to borrow.

Am I eligible for a business loan?

Your company must meet the lender's requirements to qualify. Every loan provider will have its own lending criteria, but here are the most common requirements for a UK business loan:

- You will need to be a UK resident with a business registered in the UK

- Your business will need to have been operating for at least 6 months for certain products

- You will need to have a clear purpose for the loan

- No adverse credit on your business or personal credit files, i.e CCJs, bankruptcies, liquidations, IVAs etc.

When you apply for business finance with Aurora Capital, you can get a decision on your eligibility within minutes with no impact on your credit score.

Here’s how to navigate the application process and maximise your eligibility chances.

Pros and cons of business loans

Before you apply for a business loan, it’s important to consider the pros and cons.

Pros of business loans

- They offer the financial flexibility to invest in your business

- Allows you to grow while keeping full control of your business

- You can choose between a range of loan types

- Some loans offer payment holidays if your business has cashflow problems

- Invest into the business without using your own cash flow

- You can offset the interest element of the loan against corporation tax

Cons of business loans

- The eligibility criteria can be strict

- It will add to the debt burden of your business and could impact your cash flow

- A secured business loan could put your business assets at risk if you can’t keep up with your repayments

- You may need to give a personal guarantee, which means your personal finances could be impacted

Will a business loan application affect my credit score?

Applying for a business loan with Aurora Capital will not directly impact your personal credit score.

We conduct a soft credit check during the initial pre-qualification process, which does not leave a mark on your credit report.

However, if you make a formal application, the lender will leave a hard check on your personal credit report, which would leave a mark. Your credit score will not be directly impacted for taking a loan, however if you miss or default on a payment this could affect your overall score.

We strive to minimise potential impact and ensure a transparent and responsible lending process.

Do I need to give a personal guarantee?

A personal guarantee is a legal agreement between you as a business owner and the lender which states that you’ll be personally liable for repaying the loan if your business defaults or goes into liquidation or administration.

Some lenders will ask for a personal guarantee, but it will depend on the type of loan you’re applying for and how established your business is.

How much can I borrow with a business loan?

The amount you can borrow will depend on things like the size of your business, your assets, your affordability, and how long you’ve been trading.

Typically, loans for business are available for between £10,000 and £ 2 million, but specific lenders allow you to borrow more.

Can I get a business loan if I have bad credit?

Yes, it is possible to get a business loan if you have a poor credit score, but your options may be more limited. Lenders will view you and your business as a higher risk; therefore, many will be unwilling to offer you a loan.

However, there are loans designed for those with poor credit, but the rates are often higher, and the terms can be less favourable.

What documents do I need to provide?

The documents required to apply for a business loan with Aurora Capital may vary depending on the loan program and your business's specific needs.

Generally, all that you will need to provide is:

- Last 6 months' bank statements

- Latest company accounts

- Personal and business information

Our dedicated team will guide you through the document submission process and ensure it is as convenient as possible.

How long does it take to get a business loan?

This will depend on various factors, including how much you want to borrow, the type of loan you want and the state of your business’s finances.

When you apply with Aurora Capital, the application will only take a few minutes, and we can then quickly match you with the most suitable finance option for your business. We strive to come back with a decision within 48 hours in most cases.

If accepted, you could receive the money in a matter of days or even hours. However, if your application is more complicated, for example, if you need to provide additional paperwork, it may take longer.

Can I pay the loan back early?

Yes, it’s possible to repay your bridging loan before the end of the term. Open bridging loans don’t have a set repayment date, so you should aim to pay this type of loan as soon as possible.

If there is an exit fee or early redemption charge, the typical amount would be one month’s interest payment or 1% of the loan.

Do I need a business bank account to get a loan?

All lenders will require you to hold a business bank account with them in order to qualify for a business loan.

Don’t be tempted to just get a loan from your business bank account provider without comparing the rest of the market first. Chances are you’ll be able to find a better deal elsewhere.

How much will a business loan cost?

To understand the total cost of your business loan, you need to know how much you want to borrow, the interest rate that comes with the loan, and the loan term.

The higher the interest rate and the longer the term, the more you’ll pay in interest overall. To get an idea of how much a loan could potentially cost your business, use our business loan calculator.

What is the difference between a personal and a business loan?

A business loan is made to be strictly used for the benefit of your business, such as buying new equipment, expanding your premises, or covering a cash flow shortfall.

A personal loan is designed for use by an individual for things like a big purchase or debt consolidation. Unsecured personal loans tend to have higher interest rates than business loans.

Although you cannot use a business loan for personal spending, some lenders may allow you to use a personal loan for your business. However, remember that you will be personally responsible for the loan and not your business.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)